Every Friday I prepare an Economic Snapshot – to track the Recession, pinpoint the Recovery, and help you make better decisions in your business. Subscribe here for updates by email.

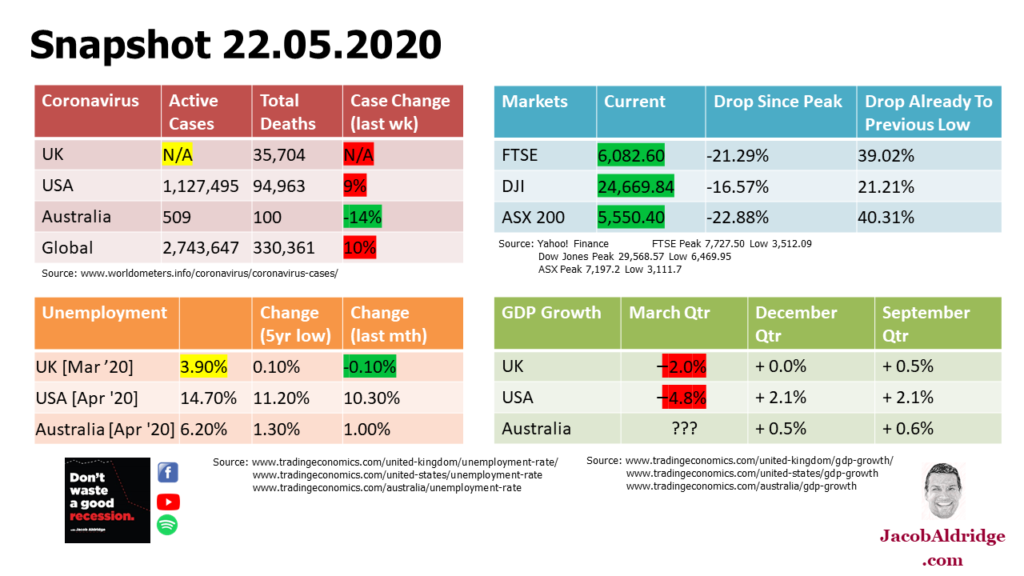

- Coronavirus LIVE Cases, Deaths, Change since Last Week

- Stockmarket Levels for FTSE, Dow Jones, ASX 200 and comparisons to the Peak and Previous Recession Low

- NEW Unemployment Rates and comparisons to Last Month and 5 Year Low

- GDP Growth and comparison to previous two quarters

- Plus this week a bonus deep dive into the rate of Active Coronavirus Case Growth across 13 different countries and globally.

Welcome to the economic snapshot for Friday the 22nd of May 2020.

This is Snapshot Number 10, the first of our new standalone programming. I am your host, International Business Advisor Jacob Aldridge. This is “Don’t Waste a Good Recession”, providing positive and practical guidance for business owners with two to five hundred employees.

You can download the Slide Deck here.

The four economic measurements that we currently look at every week:

1) We start top as we always do with the number of Active Coronavirus Cases, COVID-19.

Now this week worth noting that the UK has decided to change how it reports Recovered Cases and therefore the number of Active Cases across the UK. As a result we don’t actually have any data from the government this week, and we’re not expecting to get it until at least early June.

My estimates would be that they are continuing along the same trajectory they have been, and indeed from a percentage perspective in terms of Active Cases they track fairly closely with the US and the Global indicators which again this week continued to climb around about that 10 percent mark. Here in Australia where we have “Flattened the Curve” we have managed to decrease again.

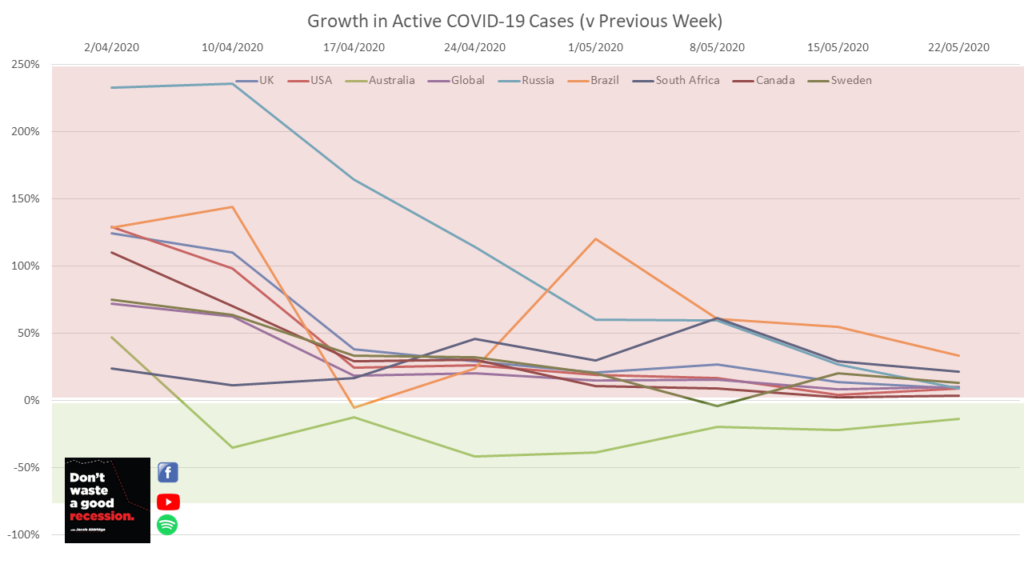

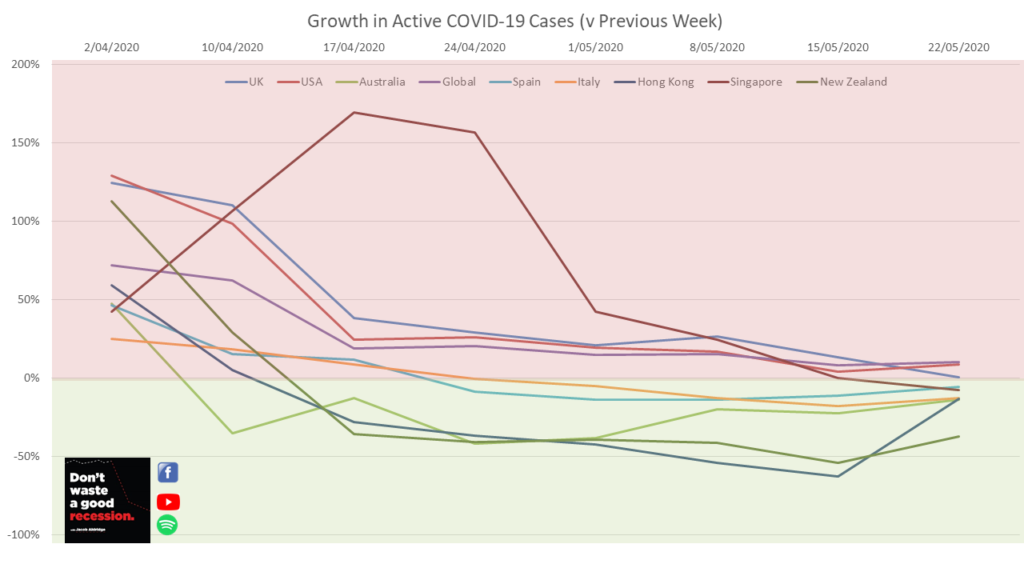

The Chart I want to dive into this week is looking at this information how it applies to lockdown, the economy and your business across those key countries and a number of others. We’re looking here at the percentage change in active cases every week. We’re not looking at cumulative cases and we’re not looking at how the actual number has changed, but looking rather at the percentage.

We’re going to break down that number into two areas: the first of which is above the line, which is shaded in red, this means that the number of active cases has increased for the week. A country that sees its numbers in the red more often than not will be climbing, we’ll be seeing more active cases week after week after week.

Below the line in the green the weeks or the countries who are seeing the number of Active Cases decline and reduce. Countries that are primarily in the green going to be seeing the number of active cases reducing significantly.

If we put first the four numbers that we have been looking at week on week since March, we have the UK the US, Australia, and then we have the Global numbers. As you can see Australia certainly stands out as the exception against those others.

While the UK, the US, and Global numbers have trended towards that zero line they have sustained week after week after week a number that’s positive, that’s in the red. This means that the number of active cases continues to climb. We look there at a number of other countries that have similarly consistently stayed in that red, Active Cases growing: Russia, Brazil, South Africa, and in that time period Canada, and even Sweden which of course is very controversial giving us a test case for how to perhaps apply a Herd Immunity and see if that makes a difference in numbers. As we can see on a percentage basis similarly tracking places like the UK and the US.

Conversely, we have a look but the baseline up there again, here are some countries that have consistently seen their numbers going into the green meaning the number of active cases is reducing week after week: Spain, Italy, Hong Kong – some of these countries that had it first, so earlier on than this chart which starts at the beginning of April – and also New Zealand which is very much starting to reopen their internal economy.

The question for you as a business owner, as a leader in your community and industry: How can a country or a region reopen if the active cases continue to climb? Especially, as we’re seeing with some of those countries, they’re climbing in spite of existing lockdown restrictions?

Even if a country does start to reopen, to relax some of those restrictions and many countries will based on the economic need or the “lesser of two evils” approach – How many people are actually going to feel confident stepping out into their communities when they know that their community or their country is sitting in the red? That the number of active cases is climbing and therefore endemic in their community? How many people are actually going to go ahead and spend money?

Because if that number is low, it doesn’t matter if it reopens. The demand won’t be there.

How many people are actually going to go to work in many industries where they feel that they are at risk of contracting this deadly disease? Because again, even if they’re allowed to go to work, if they don’t then that will have an impact perhaps on them financially but on the Supply Side of the economy and as we saw last week when we talked about how the coronavirus recession is different to a typical recession that lack of Supply one of the key things that means that this will be a deep and protracted recession.

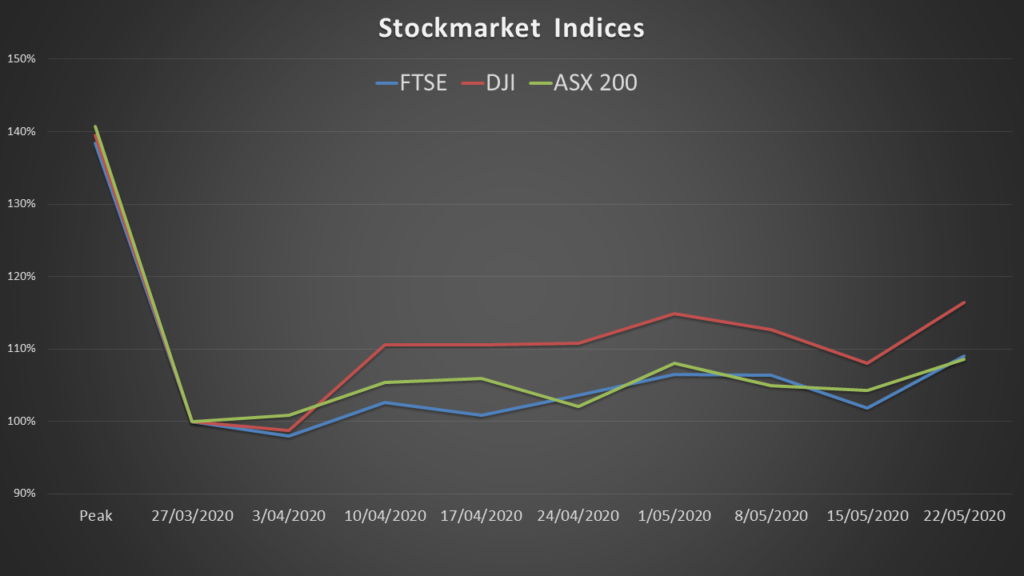

2) Moving to the other numbers for the economic update this week, all of those stockmarkets that we track were green, they were up for the week.

If we have a look at how they have progressed, we set a baseline at 100 for when we first reported on those three on the 27th of March. You can see how each came down from the peak, and how they have each climbed.

Now we track the stockmarket as a Lead Indicator of broader economic sentiment. This Recession is slightly different in that the drop in the market happened much faster and much closer to the actual drop in economic output as a result of the pandemic.

If we trust that this is a lead indicator, we can see how the market’s dropping through March led to wider economic slowdowns in April; and that does perhaps suggest that the growth we’ve seen in the stock markets in April and May so far does mean that May and June in your economy (certainly in those major economies) will bounce up off the bottom.

I certainly know that that aligns with my experience in Australia. However, if the other indicators are still pointing us towards a protracted recession we would expect those markets to start to decline in advance of the wider economy dropping.

Hopefully there might be a little bit of sun for you to make some hay in this interim period.

3) Very briefly the final two numbers for this week. The UK has finally graced us with their unemployment figures for March.

It actually went down bucking most projections! Now, that figure only includes the very first week of lockdown. The general consensus forecast is that unemployment in the UK will get to 9 percent for April, but we won’t officially learn that until late June. However in the US and Australia unemployment figures came in below some of the forecasts by around about two percent, which could mean that the UK is only going to deliver an unemployment figure for April (when they eventually do) of around 7 percent. However something like 8 million UK workers are currently on the Furlough program: this means they’re not working, but they’re being subsidized, stimulated, paid a salary by the government but they are not counted in any of those unemployment figures.

So there’s 8 million additional workers who won’t show up in that 7% or 9% and would, otherwise have been added on top. Many of them have zombie jobs. When the intervention ends, when the stimulus packages end, so – unfortunately – will their employment.

And that’s the conversation I’m having with a lot of business owners here in Australia, where I live, and around the world: this expectation that the government stimulus package has done a good job of propping things up in the short term but it cannot last forever, and when it stops and a lot of the unpreventable impacts of this Recession will start to flow into the wider economy.

4) This week no new GDP figures. We’re still two weeks away from hearing how Australia did in the March quarter. We’re expecting that to drop, Bushfires as well as Coronavirus, and really demonstrate that we are in the middle of the Coronavirus Recession.

Until next week, please Like, please Share, and please let me know your thoughts and any questions you may have about the Economic Update the impact of the Coronavirus Recession on your business.

[…] Cat Bounce?” Is the growth we’ve been experiencing in the markets, that we discussed in our economic update last week, a Bull Trap? Or is it a sign of an actual recovery in the […]